Failing to Plan

Summary

Summary

Facing a shifting retirement landscape requires careful planning. Unfortunately, far from planning with care, many Americans fail to make any plans at all — perhaps due to the complexity of calculating the money needed, the confusing array of educational resources, or because they incorrectly anticipate that they will continue to work indefinitely.

-

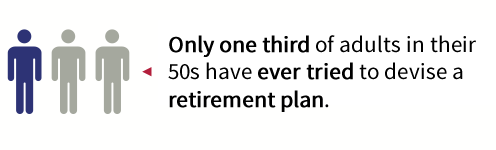

- Only 1 in 3 adults in their 50’s have ever tried to devise a retirement plan… and only 2 in 3 of those who tried, claim to have succeeded. (Lusardi & Mitchell, 2011)

- Only one-third of pre-retirees say they have a retirement plan, as well as just 57% of retirees. (Society of Actuaries (SOA), 2012)

- The typical retiree reports a financial planning horizon of just five years (median), and a general planning horizon of ten years (median). Just 2 in 10 pre-retirees say they look 20 or more years into the future when making important financial decisions. (SOA, 2012)

Failing to Calculate the Amount of Money Needed

-

- Fewer than 1 in 5 Americans over 50 have successfully created a retirement plan. (Lusardi & Mitchell, 2011)

- More than half (56%) of people haven’t attempted to calculate how much money they will need in retirement. (Employee Benefit Research Institute (EBRI), 2012a)

- Only 1 in 3 pre-retirees have a plan for how much money they will spend annually in retirement and where that money will come from. 1 in 10 says they “do not know or have not thought about it.” (SOA, 2012)

- Fewer than 6 in 10 retirees have a plan for their annual expenses in retirement and a source for the money. (SOA, 2012)

Failing to Make Use of Educational Resources

-

- More than half of pre-retirees never consult a “financial professional” for advice or guidance with financial planning. (SOA, 2012)

- Those who attempt to calculate what they will need to save use informal methods (1/4 talk to family/friends; 1/5 talk to co-workers/friends) or formal methods (1/3 use retirement calculators, seminars, or financial experts). (Lusardi & Mitchell, 2011)

- Less than half of “middle-income Americans” work with a professional advisor in retirement planning. (Center for a Secure Retirement (CSR), 2011a)

- Only 1 in 5 American workers obtain investment advice from a professional financial advisor. (EBRI, 2012a)

Incorrectly Anticipating that Work Will Continue in Retirement

Expectations:

-

- More than 7 in 10 American workers think they will continue to work part or full time in retirement. (Gallup, 2011; EBRI, 2012a)

- Approximately 14% of pre-retirees do not intend to retire because they anticipate needing the money. (SOA, 2012)

Experiences:

-

- Only 1 in 4 retirees actually work in retirement (EBRI, 2012a)

- 9% of retirees gradually reduce their hours, 9% continue to work part time, 5% continue to work full time, and 25% stop working initially before eventually returning to paid employment. (SOA, 2012)